Value of the Information

One must always distinguish between the real and potential value of the information. Of course, the information already has a certain potential value immediately after it has been collected. This value results from the properties of the information, such as accuracy, completeness, timeliness, correctness or exclusivity. The more accurate and complete the data or the information derived from the data, the higher the potential value.

This potential value is transformed into real value when the information is efficiently used in decision-making processes and contributes to increasing the level of knowledge of decision-makers in relation to their tasks. This depends primarily on the quality of the information systems, i.e. the systems that transform the information into knowledge. It should be emphasized that the context of the respective organization plays here a decisive role, including the objectives of the organization. Because even high-quality and valuable data can be useless for solving certain tasks. The criteria for assessing the usefulness of the information thus include the following: relevance, confidentiality, motivation, plausibility and transparency. Only when these subjective criteria are met does the information have not only a potential value but also a real value.

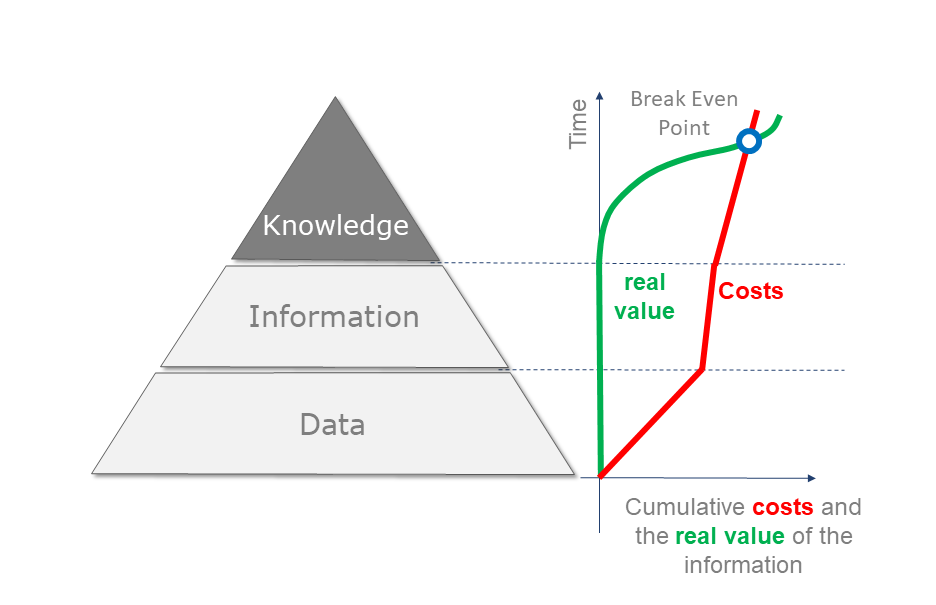

In summary, the real value of the information during the collection and management phase is initially zero. However, it increases during the application phase. The cost of information, though, arises at all stages, i.e. during its acquisition, management and provision. The efficiency (performance) of the information is thus determined – in addition to the objective quality of the data, which is regarded as a necessary (but by far not sufficient) prerequisite for the real value of the information – above all by the quality of the systems for data provision. The more efficiently the information is provided and the more it corresponds to the respective tasks and expectations of the addressees, the greater its real value becomes. These relationships are shown schematically in Figure below.

With the progress of digitization in almost all sectors of the economy and the growing importance of information, the question of the potential and real value of information is becoming increasingly important. A relatively young discipline is dealing with this question: Infonomics. The name is a fusion of the words: information and economics. Infonomics was founded by Gartner Inc. In the fundamental work “Infonomics” [1] the author D.B. Laney consistently presents information as an asset. He advocates that the rules of asset management documented in ISO 55001 should also be applied to Information Asset.

- Laney, D.B.: Infonomics, how to monetize, manage, and measure information as an asset for competitive advantage, Gartner, Inc. 2018